Ni en los extractos de pensiones ni en las circulares usuales de la Superfinanciera se le informa al cotizante cuánto han costado estos rubros. Por eso digo que son unos costos ocultos, hidden pension fees. Por supuesto, para estimar su efecto, debemos saber su monto, específicamente, su tamaño comparado con el total bajo administración, cada año. Algo tiene que ser, no puede ser 0%. Si es 0.25%, creo que no es preocupante.

Véase cómo el Departamento del Trabajo en los Estados Unidos se nota muy preocupado por costos del 1%:

Middle class economics means that Americans should be able to retire with dignity after a lifetime of hard work. But loopholes in the retirement advice rules have allowed some brokers and other advisers to recommend products that put their own profits ahead of their clients' best interest, hurting millions of America's workers and their families. A system where firms can benefit from backdoor payments and hidden fees often buried in fine print if they talk responsible Americans into buying bad retirement investments—with high costs and low returns—instead of recommending quality investments isn't fair. A White House Council of Economic Advisers analysis found that these conflicts of interest result in annual losses of about 1 percentage point for affected investors—or about $17 billion per year in total. To demonstrate how small differences can add up: A 1 percentage point lower return could reduce your savings by more than a quarter over 35 years. In other words, instead of a $10,000 retirement investment growing to more than $38,000 over that period after adjusting for inflation, it would be just over $27,500.

In February, the President directed the Department of Labor to move forward with a proposed rulemaking to require retirement advisers to abide by a "fiduciary" standard—putting their clients' best interest before their own profits. […]

Summary of Today's Action to Protect Retirement Savers by the Department of Labor

Today, the Department of Labor issued a proposed rulemaking to protect investors from backdoor payments and hidden fees in retirement investment advice.

- Backdoor Payments & Hidden Fees Often Buried in Fine Print Are Hurting the Middle Class: Conflicts of interest cost middle-class families who receive conflicted advice huge amounts of their hard-earned savings. Conflicts lead, on average, to about 1 percentage point lower annual returns on retirement savings and $17 billion of losses every year.

- The Department of Labor is protecting families from conflicted retirement advice. The Department issued a proposed rule and related exemptions that would require retirement advisers to abide by a "fiduciary" standard—putting their clients' best interest before their own profits.

- The Proposed Rule Would Save Tens of Billions of Dollars for Middle Class and Working Families: A detailed Regulatory Impact Analysis (RIA) released along with the proposal and informed by a substantial review of the scholarly literature estimates that families with IRAs would save more than $40 billion over ten years when the rule and exemptions, if adopted as currently proposed, are fully in place, even if one focuses on just one subset of transactions that have been the most studied.

https://www.dol.gov/ebsa/newsroom/fsconflictsofinterest.html

Por ello, le pido a las AFP, a la Superintendencia Financiera y a la Unidad de Regulación Financiera que tengan un dato claro sobre estos gastos. Cómo es posible que en la discusión actual sobre Reforma Pensional no se crea que la eficiencia del sistema deba examinarse.(*)

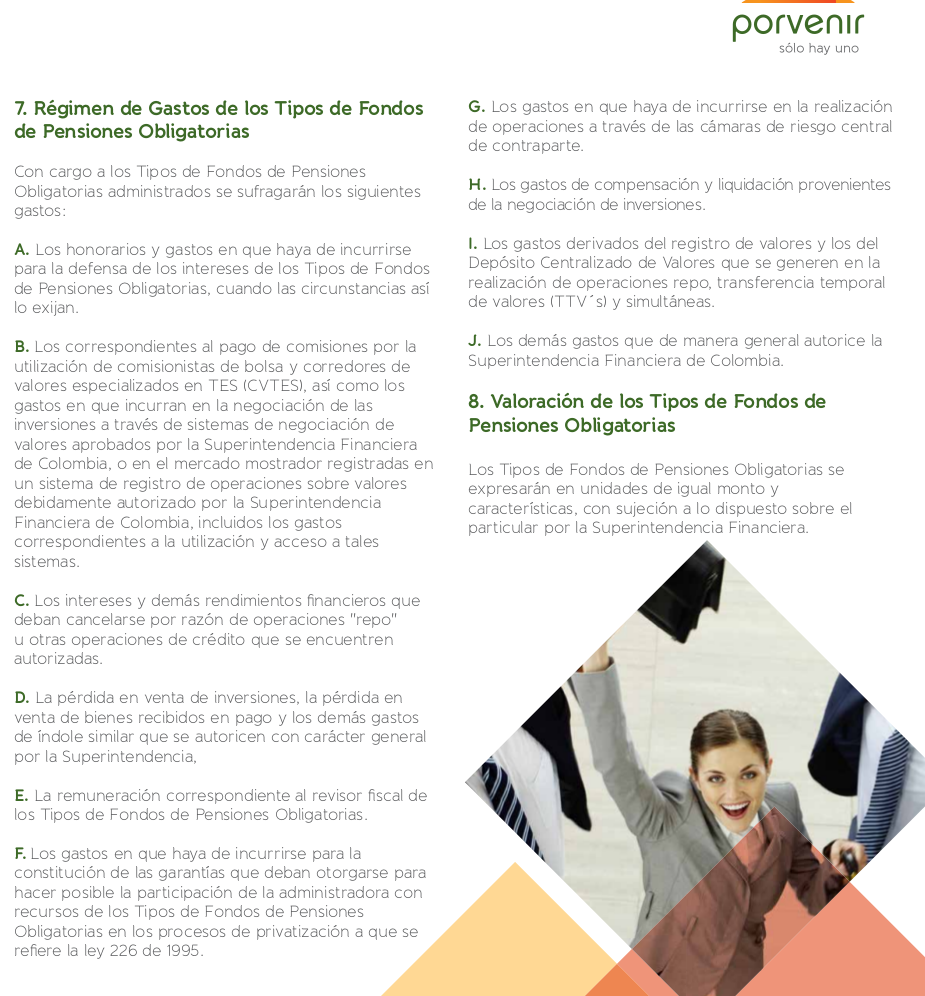

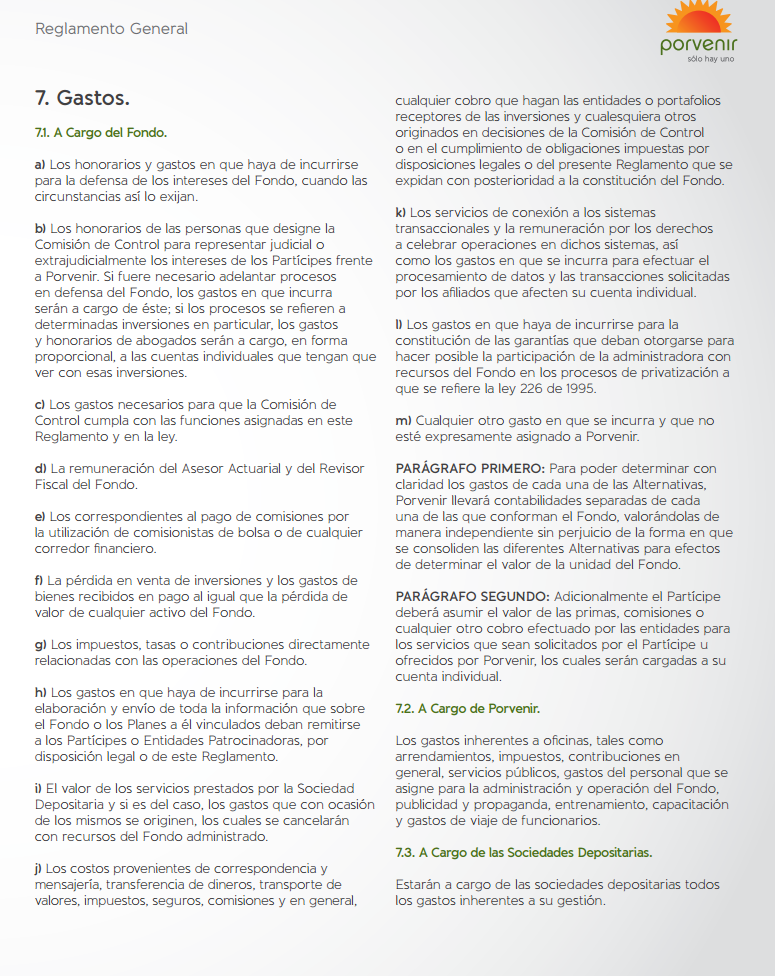

Pero todo este tiempo pensaba que esos gastos admisibles eran sólo propios de los Fondos Obligatorios. Que en los Voluntarios, la comisión sobre saldo compensaba por todo (menos, por supuesto, el Expense Rate de los ETFs). Para los carteras internacionales, si la comisión fuera del 3.5% anual y el portafolio usara fondos con un expense rate anual de, digamos, 0.5%, fondos voluntarios, por ejemplo, el lastre total sería de aproximadamente 4%.

¡Oh sorpresa: los fondos voluntarios también padecen de costos ocultos!

Del Reglamento del Fondo de Pensiones Voluntarias de Porvenir:

No sé todavía su proporción y efecto. Pero caray.

* Alcides Vargas, Presidente de Colfondos: “Los temas que debe tener en cuenta la reforma pensional son la inequidad, los subsidios mal focalizados en el régimen público, la baja cobertura y la informalidad”. (http://www.larepublica.co/%C2%BFqu%C3%A9-esperan-los-fondos-de-pensiones-de-la-pr%C3%B3xima-reforma-pensional_405266)

No hay comentarios.:

Publicar un comentario